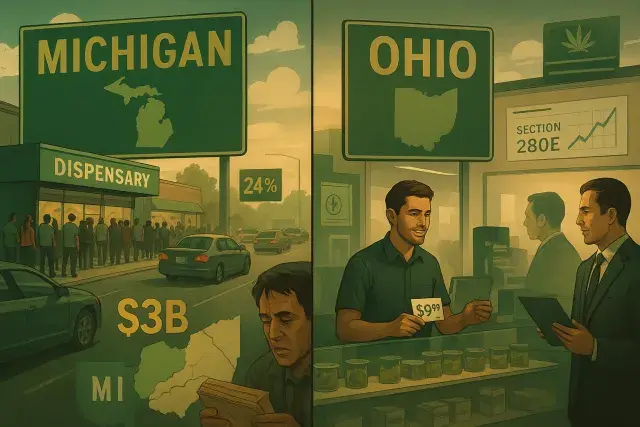

Michigan moves more cannabis than any other state in the Great Lakes region - more than $3 billion in annual sales - yet Ohio's younger adult-use market may be quietly building the stronger business foundation. Higher retail prices, healthier operator margins, and a less saturated competitive field are giving Ohio's licensed industry a financial profile that investors may find increasingly attractive, particularly if federal rescheduling reduces the tax burden that has hammered cannabis operators nationwide for years.

Two Markets, Two Very Different Operator Realities

The gap between Michigan and Ohio is not simply about volume. It reflects two distinct market conditions that produce very different outcomes at the dispensary level.

Michigan's competitive intensity is well documented. Abundant licensed cultivation, aggressive retail competition, and years of wholesale price compression have produced some of the lowest consumer prices in the country. For operators, that means thin margins - and in many cases, sustained pressure on cash flow. Growers facing oversupply have watched wholesale prices drop to levels that make profitability genuinely difficult. Retailers have competed largely on price, which attracts customers but does not build durable margin structures. Michigan's new 24% wholesale marijuana tax, which took effect January 1, added another layer of cost to an already compressed supply chain.

Ohio's situation runs in the opposite direction. Consumers pay more - often significantly more than Michigan shoppers - and that pricing differential has allowed many Ohio operators to maintain balance sheets that look considerably healthier than their Michigan counterparts. A newer market with fewer licensed operators generally means less downward pressure on wholesale pricing and more room for retailers to protect their margins. That's not a permanent condition; as Ohio's market matures and additional licenses enter, pricing will face the same gravitational pull Michigan has already experienced. But right now, Ohio operators are collecting revenue per transaction that Michigan operators can only read about.

Border Traffic, Retail Geography, and the Cross-State Consumer

One reason Michigan's sales volume has stayed so high is geography - specifically, the retail corridors that sit directly on Ohio's doorstep. Dispensaries in Monroe have functioned as a destination market for Ohio consumers willing to drive for lower prices and broader product selection. New Buffalo retailers near the Indiana border operate on a similar premise: the price differential across state lines is wide enough to make the trip worthwhile for regular consumers.

Here's the catch, though. Cross-state consumer traffic is a volume driver, but it's a structurally fragile one. If Ohio's adult-use market expands its licensed footprint, prices moderate even incrementally, or new dispensaries open closer to the Michigan border on the Ohio side, that customer flow could slow. Michigan retailers who have built their business models around destination shoppers from neighboring states are exposed to a competitive variable they do not control.

In practice, the Monroe market has been one of the most watched retail environments in the Midwest precisely because it crystallizes how cannabis economics play out across state lines. Volume is there. So is real vulnerability.

Federal Rescheduling and What It Could Mean for Operator Economics

The U.S. Department of Justice and Drug Enforcement Administration have moved state-licensed medical marijuana into Schedule III and have scheduled a broader cannabis rescheduling hearing beginning June 29. The operational significance of that proceeding extends well beyond regulatory symbolism.

For cannabis operators, Section 280E of the federal tax code has functioned as a structural disadvantage with no analog in conventional retail. Because cannabis remains federally controlled, licensed businesses cannot deduct ordinary business expenses the way a hardware store or pharmacy can. The result is an effective tax rate that bears no relationship to actual profitability - operators have been taxed on gross revenue figures that would make most small-business owners walk away from the table. Rescheduling to Schedule III would not automatically eliminate 280E exposure, and the legal mechanics of how rescheduling interacts with existing tax code provisions remain contested. But the directional implication is real: any federal reform that loosens the 280E stranglehold frees capital that is currently flowing to tax bills rather than payroll, equipment, inventory, or expansion.

The question worth asking is where that freed capital goes. Michigan has the infrastructure - established cultivation operations, experienced retail staff, seed-to-sale compliance systems already running at scale, and a consumer base that is among the largest in the country. Ohio has the margins. If 280E relief materializes and investors are evaluating where to deploy capital in the Midwest, a market with stronger per-unit profitability and meaningful growth runway is a different conversation than a mature market where operators are already fighting for fractions of a point.

What Operators and Investors Should Be Watching

The competitive tension between Michigan and Ohio is ultimately a story about which market conditions produce more durable cannabis businesses - and that question does not have a clean answer yet.

Michigan's scale is real. Its brand recognition among cannabis consumers in the region is built on years of cultivating a high-volume, accessible market. Multi-state operators with Michigan licenses are not abandoning them. But scale without margin is a treadmill, not a foundation, and some investors who entered Michigan's market during its high-growth phase have had to reckon with that math.

Ohio's advantage is fragile in its own way. Higher prices invite competition, and a less saturated licensing environment will not stay that way indefinitely. The regulatory decisions Ohio makes over the next two to three years - around license expansion, vertical integration permissions, social equity access, and tax structure - will do as much to shape its investment profile as federal rescheduling ever could.

What's striking here is that both states are, in a real sense, entering a new phase simultaneously. Michigan spent the better part of a decade competing against its own illicit market. Ohio is still in early-stage adult-use development. Federal rescheduling, if it progresses, resets the financial environment for both. The operators who understand the difference between volume and profitability - and build accordingly - are the ones who will be worth watching when the next round of Midwest cannabis investment gets written.